This shows that a huge portion of businesses are still vulnerable and are not on top of financial processes, or do not have adequate checkpoints and guardrails. These simple steps can help with compliance, reduce risk, and boost overall productivity by simply making many tasks easier.

Robust financial controls enable companies to have financial stability and reduce the risk of fraud from occurring, while generating accurate accounting and financial data that can be used to aid agile decision-making.

Research commissioned by PwC has shown internal financial controls do indeed work – two-thirds of organisations that experienced fraud discovered their most disruptive incident through financial controls. No matter this size of your business, now is the time to build good habits and put these essential steps in place, instead of putting it off.

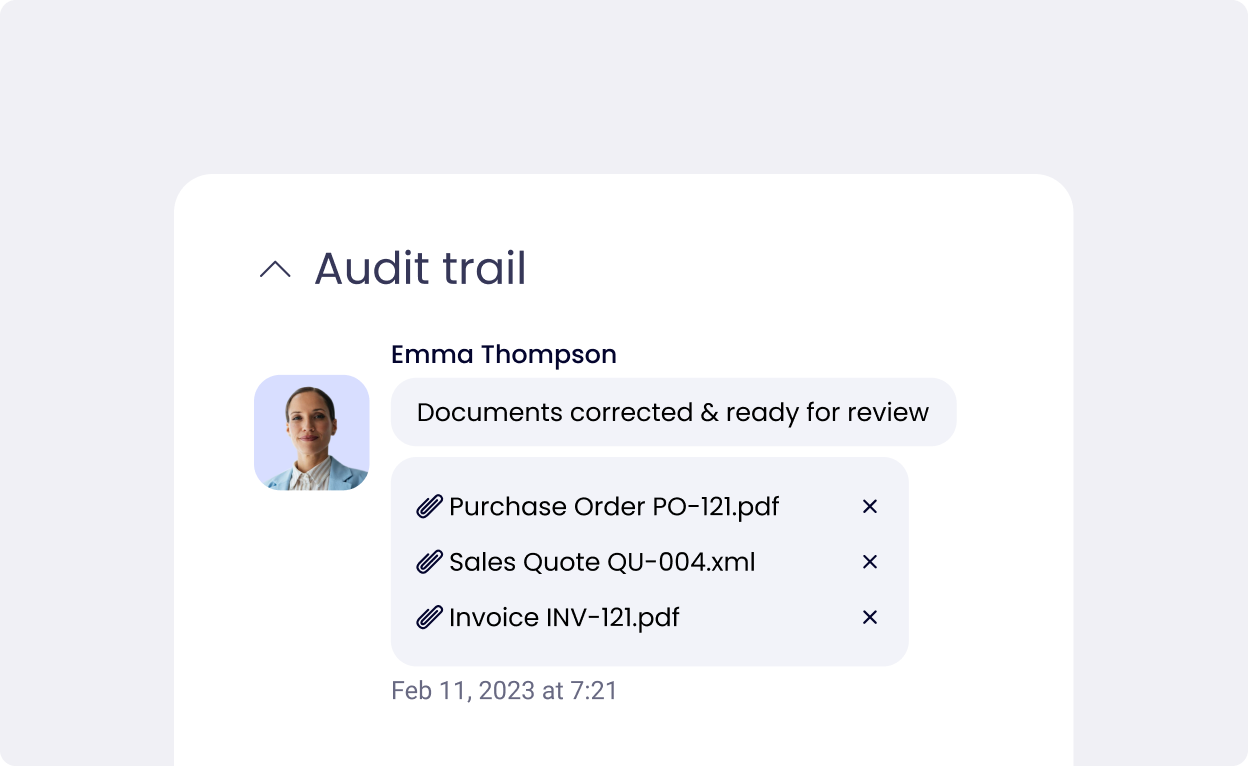

Financial controls are policies and procedures that are put in place to keep financial records in check and protect company assets. Along with preventing or detecting accounting errors, they also help find and deter fraud, such as account skimming, misappropriation of assets, or false expense claims.

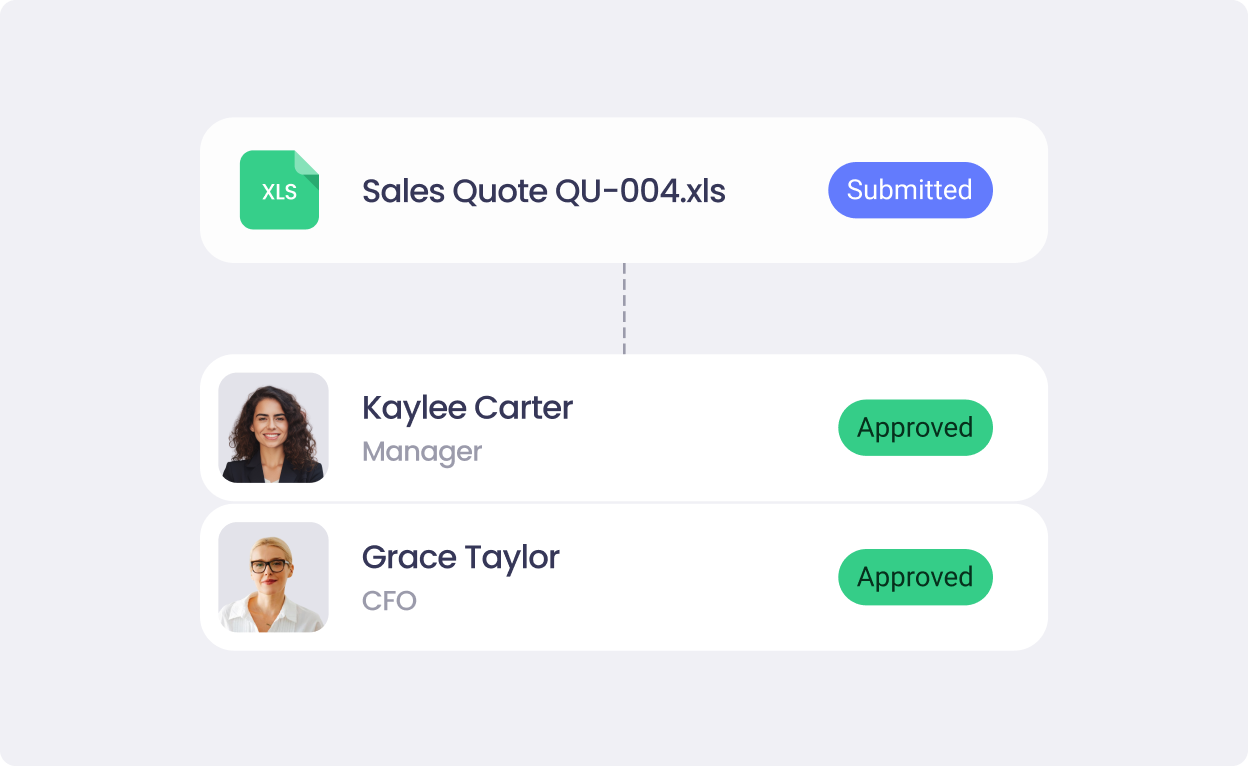

Most larger organisations have fairly extensive financial controls due to the size of their teams. They may implement stricter controls, such as automated workflows and multi-tiered approvals, to maintain oversight over complex financial processes. Smaller businesses, on the other hand, tend to have less rigor around these processes – it’s not uncommon for one person to handle most financial tasks. For example, a small business might use financial controls to prevent a single employee from both processing and approving payments, reducing the risk of fraud. Adding controls not only makes their lives easier and the business safer in the long term, but also those of their accounting and bookkeeping partners.