Most financial risk happens before a payment is made - yet most finance tools only show you what happened after the money has left. How your business controls spend, approvals, and payments is the difference between your finance team being in control or not.

In finance, a lot of focus is put on Money In - the revenue coming in from new customers, upsells and subscription fees. But for every healthy business, there’s something just as important (and sometimes more so): Money Out.

Money Out is the practice of treating outgoing spend as a managed lifecycle. It requires visibility, control, and approval at every stage - not just reconciliation after payment.

In this blog, we’ll outline what a Money Out process looks like when it works, and the problems and costs that occur when it doesn’t.

The Money Out lifecycle for AP

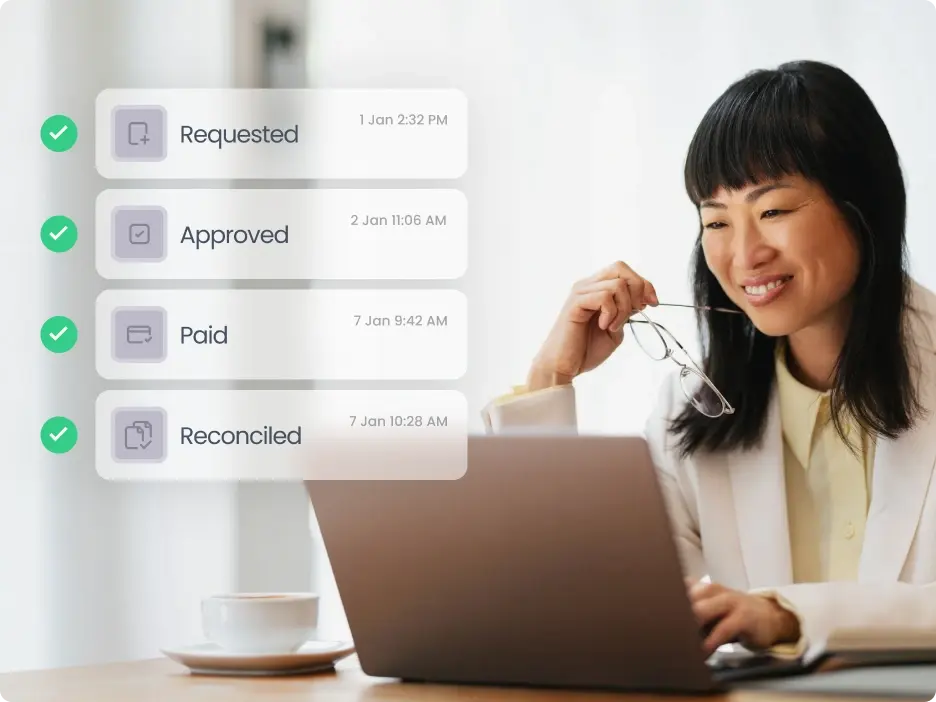

Money Out encompasses the entire lifecycle of outgoing business spend, from the moment somebody makes a request to buy something, through approvals and payment, to finance reconciliation.

This lifecycle includes five key stages:

Request: Someone identifies a business need and submits what's being purchased and why

Approval: The right people review and authorise the spend based on policy and budget

Payment: Money moves from the business to the supplier at the right time

Reconciliation: The transaction is matched to budgets and recorded in the accounting system

Audit: A complete, timestamped record proves who approved what, when, and why

But what’s wrong with traditional ‘expense” thinking?

Traditionally, businesses manage outgoing spend in a fragmented way: purchase requests arrive with no warning, approvals happen in email threads, bills get paid straight from the accounting system, and visibility only comes after the money is gone.

This can work in the early days of a small start-up, but as the business scales, so does the element of risk. This type of fragmentation leads to limited oversight before spending happens, inconsistent approval processes, and errors, delays, and duplicate payments. As a result, there is little accountability across teams and budgets are frequently exceeded through lack of visibility.

The current status quo - aka a failing Money Out system

Here’s a typical scenario that we see with a lot of businesses we speak to:

A medium-sized business receives 200 - 400 invoices a month.

Intake: Invoices arrive via a shared finance email or are physically handed to the bookkeeper.

Validation: The bookkeeper manually checks the invoice against a spreadsheet of "Approved Budgets" or tries to find a matching purchase order in a different system.

Routing: The bookkeeper attaches the PDF to an email and sends it to a Department Head for approval.

Thebreak: If the Department Head is busy, the email is buried. The bookkeeper has no central view of "who has what," so they spend around two days a week manually nudging people via Slack or follow-up emails.

Payment: To avoid late fees, the finance manager sometimes pays invoices that haven't been fully signed off, assuming they are "probably fine."

There are a number of critical indicators that demonstrate the above process is a failing process.

Based on data from ApprovalMax prospect calls, with this process, a business with a broken Money Out process spends an average of 10–15 minutes per invoice just on administrative routing and data re-entry.

Invoices take 14+ days to move from "received" to "ready for payment" - creating approval lag that slows the entire business.

The hidden costs add up fast: up to $40k per year in wasted time, calculated purely from the cost of an employee chasing approvals. And manual data entry creates a 1% error rate, leading to duplicate payments or coding to the wrong department.

How can a great Money Out process make a difference?

A well-managed Money Out process helps brings together:

1

Spend control

Ensuring every outgoing payment is reviewed and approved by the right people before it happens. For example, a $5000 software subscription doesn’t get approved by someone who can only authorize $1000.

2

Process consistency

Replacing ad hoc approvals with structured, auditable workflows that scale as the business grows.

3

Visibility

Giving finance teams real-time insight into what’s been requested, what’s been approved, and what’s about to be paid. This doesn’t happen after the fact, but before the money goes out.

4

Confidence

Allowing your business to pay faster and more efficiently, without sacrificing control or compliance. Every approval, payment, and decision is automatically documented, so when it’s audit time, or you need to investigate a discrepancy, you have a complete trail.

Why a strong Money Out process matters more than ever

As a business scales, the process of money leaving it becomes more complex. There are more spend categories, more approvers, more systems… and more risk.

Without a clear Money Out framework, finance teams are forced into reactive mode: chasing approvals, fixing mistakes, and explaining surprises.

By treating Money Out as a strategic discipline, businesses can reduce financial risk, strengthen internal controls, improve cash flow planning, and enable faster, more confident decision-making.

Money Out and modern finance teams

For modern finance teams, Money Out isn't about slowing the business down. It's about creating guardrails that allow the business to move faster.

When Money Out is clearly defined and well-managed, teams know what they can spend and when. Approvals happen quickly and consistently. Payments are accurate, timely, and auditable. And finance regains control without becoming a bottleneck.

The question isn't whether you manage Money Out. You already do. The question is whether you're doing it with clarity, confidence, and control - or scrambling to catch up after the money's already gone.

How ApprovalMax can help

Ready to move your finance team from firefighting to forward-thinking? Book a demo today.

ApprovalMax is a trusted Xero, Quickbooks and NetSuite partner who helps finance teams implement structured approval workflows and financial controls across the entire Money Out lifecycle - not just at the point of payment.